Carbon Coin

... faceless bureaucracies to the climate rescue?

When we think about “stopping” or at least “slowing” climate change, we will get nowhere without changing a lot of what people do today.1

But not only do people generally not like to change, but they definitly don’t like changing for the worse.

A lot of the proposed “solutions” for climate change will be perceived as exactly that: a change for the worse. The loss of their beloved car, less of the food they like to eat, less travel, especially by air, less A/C in summer, less heating in winter, less discretionary spending, fewer children.

For a lot of people around the globe, this is not unpleasent, but devastating, even deadly, because they have just recently clawed their way out of abject poverty.

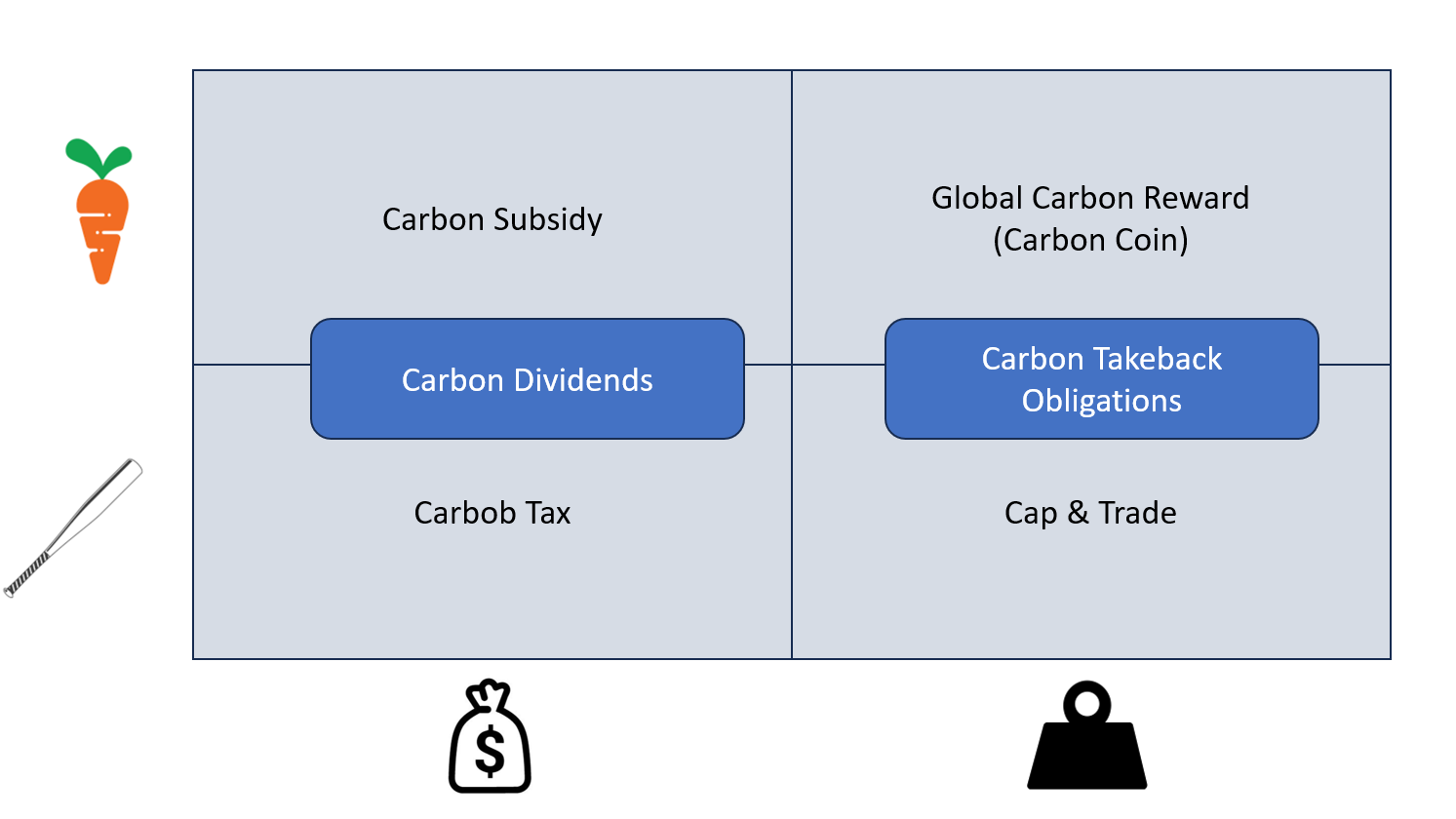

Getting people to do things they don’t want to do requires an incentive: either a stick or a carrot. Or both.

While I have written extensively about the “stick-y” side of this, for example about cap&trade or carbon taxes. and mixed forms, like carbon dividends or carbon takeback obligations, I haven’t yet delved into the “carrot-y” side of things. Until today.

What is the idea behind carbon coins?

In Kim Stanley Robinson’s “The Ministry for the Future”, the “carrot” of carbon pricing, the Carbon Coin, alternatively called Carbon Quantitative Easing or Global Carbon Reward, intruduced by Chen et al., features promiently as a major part of the that fictional future’s success in reigning in, maybe even reverting climate change.2

The proposal is quite far reaching and needs the participation of ideally all, but at least 20-40 central banks of the largest economies, representing 80-90% of the world economy by GDP.

These central banks would cooperate and create a new currency, a carbon coin, which is nominated in 1 tCO2eq mitigated for a 100-year duration.

While the carbon currency would not be legal tender in any country, the central banks would make sure that it can be exchanged for national currencies, guaranteeing a rising real floor price.

The future floor price of carbon coins is rising according to a known schedule. There is no upper limit on the spot price of the carbon coin, but it will never fall below the floor price.

This is ensured by the central banks, which would have to use quantitative easing3 to defend the floor price in their respective national currencies.

The carbon coin will be managed by a new supranational authority, called the carbon exchange authority (CEA). It is a self-funded administrative system, which recoveres its costs through fees and commissions that will be charged to entities that earn a carbon coin.

This authority will issue a carbon coin, if an entity mitigated 1 tCO2eq in accordance with the authority’s standards4. It also ensures the accountability, fungibility and transparency of the carbon currency.

Relying on this, central banks are not required to undertake any technical assessments of climate mitigation services - they just have to trust the CEA.

The carbon coin could also be used as an index for the profitability and effectiveness of low-carbon investments. By construction, the amount of carbon coins accounts for the sum of all mitigated carbon.

Carbon coins work similar to a carbon offset, where the buyer (CEA) immediately retires them permanently. The coin is not redeemable for mitigated carbon.

What are the benefits of this idea?

By giving the carbon currency a predictably rising floor price, it will attract investment demand from institutional investors and households.

Investments by the latter in a carbon currency would increase the average savings rate and reduce household consumption. Private demand for carbon coins will be high, when the price floor rises quickly. This means that this demand can be stimulated by the central banks.

Proponents of the carbon coin claim that the coin is not a subsidy, because:

the coin is issued as “token”, not as a national currency,

it is funded by international monetary policy, and not through fiscal spending,

the coin is performance-based, while subsidies are not necessarily so.

They also claim that this funding model does not result in any direct costs for governments, businesses or citizens. That is because instead of raising taxes, the proposal raises inflation. The mitigation cost will be “hidden” via the foreign exchange currency market, where participating countries’ national currencies are devalued relative to the carbon currency.

This supposedly helps to overcome barriers to decarbonization of the world economy, like monetary, financial, political and legal systems5.

Why would you want a carbon coin?

To justify the creation of the carbon coin, Chen at al., formualted an alternative economic theory, called “Holistic Market Hypothesis”, which claims that the market failure in carbon is not a classical market failure, because the systemic risks associated with the anthropogenic carbon balance are so unusually large that there is the need for a second, positive externality, called the “Risk Cost of Carbon” (RCC) to be internalized to fix the failure.

This positive externality should be managed independently of and additionally to carbon taxes, cap&trade, etc., which internalize the negative externality. Internalizing the positive externality is supposed to create a new global carbon market that has the qualities of a global public good, i.e. non-rivalrous, non-excludable, and available worldwide.

The RCC is conceptualized as the price a virtuous actor has to pay to do a quantifiable amout of good (= ”save the world via fixing the anthropogenic carbon balance”) against the resistance of societal systems. Tomorrow’s risks are converted by central banks into today’s profits for the virtuous.

The goal of the carbon coin is to achieve net-zero, maybe even net-negative emissions.

Typically, the relationship of carbon emission to population, economy and energy is modeled by the Kaya identity,

where F represents the global CO2 emissions from human sources, P is the global human population, G is world GDP and E is global energy consumption. G/P is the GDP per capita, E/G is the energy intensity of the GDP and F/E is the carbon footprint of the energy.

With △Q as the amount of globally, verifiably mitigated CO2, and ω as the percentage of that removal that happens outside of the normal economy (and is therefore not part of G), i.e. is remunerated with carbon coins, a modified identity can be formulated as:

Chen et al. assume that ω△Q could be large6 .

Given the modified formula, it can easily be seen that humanity’s carbon emissions can be reduced by reductions in global population, a decrease of the average carbon intensity of goods and services (F/G), a decrease of the average carbon intensity of the used energy (F/E), or by increases in global cabon dioxide removal, which the carbon coins are supposed to stimulate.

Policies focused on reducing P, G or E ( these are the fewer people, less wealth and less energy of the introduction) in absolute terms, are called degrowth. These policies are considered by some7 as a less risky, yet obviously politically challenging pathways to F≤0.

What’s the rub?

Introducing a carbon coin necessitates the creation of a supranational and powerful organization, as well as the lasting cooperation of all the major central banks.

Some governments would certainly regard this as a severe loss of souvereignty. Carbon taxes, on the other hand, can be created and enforced at an appropriate level locally via border adjustment taxes. The revenues of these taxes can be used by governments as they see fit (redistribution via dividends, investments in clean RD&D, etc.).

By design, the prices of carbon coins are set independently by the CEA and costs are imposed via inflation, without democratic consent, which might similarly be regarded as a disenfranchisement by voters. While carbon dividends are a straight forward and equitable redistribution mechanism for a carbon tax, there is no obviously associated compensation mechanism for the world’s poor to counteract the inflationary effect caused by carbon coins. Any policy aimed at propping up their spending power voids the argument that these coins do not produce costs for governments or citizens.

Taking something that market participants don’t value and putting it profitably right at the center as the measure of value, nullifies market participants’ preferences. There is no guarantee that doing so will not distort the markets for food, housing, energy, health and educational services etc. and no government can stop the CEA from creating too much inflation for their poorer people.8 “Distorting markets” in this context could for example constitute large landowners exchanging their food production crops for some inedible, fast-growing grass, to pyrolyze it after the harvest and sequester the CO2 as the reulting oily residue. Something similar (ethanol subsidies) has sparked a huge debate around the perverse incetives of using crops for biofuel instead of as food. Depending on the price of the carbon coin, it could also prove to be much more profitable to install for example solar-powered direct air capture devices, instead of using the same solar power to lift poor people out of poverty.9 In fact, a huge demand for sequestration services could drain resources from the digging, drilling, construction, chemical, semi-conductor and similar industries, raising the price for their respective goods well above the already “carbon coin”-boosted general inflation rate.10

The justification for the magnitude of this intervention is the invention/invocation of a new economic theory and a modification of the concept of dealing with externalities, which does not appear to be mainstream economics.

Summary

Carbon coins are a top-down mechanism that circumvents (by design and intent!) democratic, financial, monetary and legal norms.

It would probably benefit people with available capital11 seeking for a safe haven, investing profitably in a guaranteed, arbitrarily multipliable asset. While the profits are privatized, (at least without any additional interventions) the costs are socialized highly regressively via general inflation, and probably cost increases in industries especially important for poorer people.

I don’t see any immediate scenario for their implementation, because I don’t believe that governments or electorates would give away that much power to an unelected entity, but I am not sure that I would be happy, if there were a pathway.

While carbon coins seem marginally less draconian than outright degrowth policies, the creation of an authority, shielded from market or democratic feedback, able to create arbitrarily large sums of money, tasked not with ensuring human flourishing, but with carbon removal, has to be viewed with the highest degree of skepticism for its effect on the people.

It is a proposal befitting Sowell’s “anointed”.12

.. or inventing/innovating a firm, clean power source cheaper than coal. Possible contenders include nuclear fission/fusion, geothermal, solar thermal, etc. This would reduce the economy’s carbon intensity.

Other interventions in the book include:

universal basic income,

universal basic services,

nullifying all low-tax jurisdictions,

tracking all money and transaction on a blockchain,

using different metrics than GDP to measure economic value generation,

enforcing a maximum spread of income,

enforcing a maximum allowed amount of personal wealth - confiscating everything above a threshold,

a vast international, undemocratic bureaucracy funding covert operations,

unknown covert groups or indivuals kidnapping the WEF in Davos, as well as

shooting down dozens of planes to make people afraid of flying, infecting (or claiming so) millions of cattle with mad cow disease to make people eat less beef, blowing up power plants, sinking commercial ships and murdering executives of fossil fuel companies (talking to them “felt to her like she was negotiating to buy off terrorists who had explosive vests strapped around their waists, and were saying to her and to the world at large, pay us or we blow up the world.” Robinson, Kim Stanley. The Ministry for the Future (S.238). Little, Brown Book Group. Kindle-Version.).

The rationale for these interventions is fear of crossing a threshold in the “wet-bulb temperature” (measuring a mix of air temperature and humidity), which (in the fictional world) killed twenty million people, but does very fortunately appear to not translate from theory to real world, as well as the idea of irreversible tipping-points, which are speculated to create postive-feedback in global warming.

Given the list of interventions above, the assessment of Seaver Wang (@wang_seaver), author of a rebuke of the ideas of climate tipping-points, seems accurate: “Taken at rational face value, the feeling that the planet is just years away from sliding beyond a catastrophic point of no return invites unproductive fatalism.”

Also known as “printing money”.

This could by achieved by retiring production of fossil fuels, installing CCS technology to an already existing plant, converting a coal plant to a nuclear plant, changing carbon intensive production processes, like converting coke-fired blast furnaces for steel to hydrogen, using different farming techniques, or carbon dioxide removal and sequestration.

i.e. majority votes, plebiscites, constitutions etc.

This assumption seems justified: given the strong financial incentives, △Q might be large. Additionally, given that removed carbon, for examle as some oil or brine deep underground or a slightly more weathered rock does not appear to have any economic value to market participants today, ω might be close to 1.

For example: Keyßer LT, Lenzen M. 1.5 °C degrowth scenarios suggest the need for new mitigation pathways. Nat Commun. 2021 May 11;12(1):2676. doi: 10.1038/s41467-021-22884-9. PMID: 33976156; PMCID: PMC8113441. Link.

Given the assumed stakes (global annhilation), this might still be worth the cost for some proponents.

The tendency of Western climate activists to disregard any ambitions of poorer countries, especially in Africa and South East Asia, to increase their energy consumption to increase their standard of living, has variously been described as a continuation of the worst aspects of colonialism. For example here, or here.

Which calls into question Chen at al.’s modelling of the carbon coin economy as independent of the “regular” economy

commonly called “the rich”

[The anointed’s preferences] are to supersede the preferences of everyone else that the particular dangers they fear are to be avoided at all costs and the particular benefits they seek are to be obtained at all costs. Their attempts to remove these decisions from both the democratic process and the market process, and to vest them in obscure commissions, unelected judges, and insulated bureaucracies, are in keeping with the logic of what they attempting.

They are not seeking trade-offs based on the varying preferences of millions of other people, but solutions based on their own presumably superior knowledge and virtue." - Thomas Sowell